Helpful miscellaneous articles

regarding our retirement plan and planning.

Like you, I review my retirement nestegg and plan from time to

time. Recently, I went though some

continued education for some credentials I maintain and it occurred to me that

we all could use a review about these issues.

So with your help, we will share and post articles and info that may be

helpful and of interest to many of you in this section.

Timeless

Ways to Protect Yourself From Inflation

By

Updated January 02, 2022

Reviewed by

Fact checked by

In addition to

death and taxes, inflation is another

phenomenon that we can expect with near certainty over a period of time.

The U.S. has

actually gone through many brief periods of deflation, but in general, economic

progress is accompanied by inflationary pressures. Inflation may occur when

there is too much money in the system, which leads to an escalation in the

price of goods. Of course, if a household's two primary sources of wealth

creation—asset and income appreciation—rise at a rate equal to or greater than

inflation, the negative effects of inflation are neutralized.

Yet, as we've

seen time and again, that usually is not the case. While the minimum wage has increased, the

overall price of goods has outpaced the average salary increases of recent

years.1

Practice

trading with virtual money

Find out

what a hypothetical investment would be worth today.

SELECT A STOCK

TSLA

TESLA INC

AAPL

APPLE INC

NKE

NIKE INC

AMZN

AMAZON.COM, INC

WMT

WALMART INC

SELECT

INVESTMENT AMOUNT

$

SELECT A

PURCHASE DATE

CALCULATE

The Worst Tax

Inflation is

often referred to as the "worst tax" because its effects go unnoticed

by most people. Hypothetically, earning 4% in a savings account while

inflation grows at 7% makes many feel 4% richer. In fact, they are 3%

poorer.

That's

why it's important for households and investors alike to understand the

causes and effects of inflation, and how to plan so as to ensure that their

assets maintain their purchasing power.

Here are three

investment approaches everyone should consider as ways of protecting their

hard-earned wealth from the ravages of inflation.

Although inflation may be less dramatic than a stock market

crash, it can be more devastating to your portfolio.

Invest in Stocks

Despite the

lack of confidence most people express about stocks, owning some equities can be a very good way to combat inflation. Think of your

household as a business. If a company cannot properly invest its money in

projects that will deliver a return above its costs, then it, too, will fall

victim to inflation. The basic premise of business success is that corporations

will sell their goods at increasing prices, which will lead to elevated revenues, earnings, and inevitably, stock prices.

Some of the

best stocks to own during inflation would be in companies that can increase their

prices naturally during inflationary periods. Commodity resource companies are

one example. Products like oil, grains, and metals enjoy pricing power during

periods of inflation. The prices of these items tend to go up as opposed to,

for example, the price of a computer, which is subject to manufacturer and

distributor price adjustments.

Still, price

increases aren't enough to protect against inflation. If a company experiences

rising expenses, price increases alone are not enough to maintain equity

appreciation. That's why grocery stores, which may benefit from an increase in

food prices, may also suffer from an increase in their cost of

goods sold.

Look to invest

in businesses such as commodity firms or

healthcare companies that possess the strongest profit margins and,

generally, the lowest cost of production. Finally, never underestimate the

value of dividends during periods of inflation. Dividends increase the total

return of a portfolio.

Invest in a Home

When done for

the right reasons, like buying a home to live in, real estate is always a good

investment. Problems occur when a buyer's goal is to flip the property they just

bought at a profit. Although experienced real estate investors are able to

find hidden values in

properties, the average person should focus on purchasing a home with the

intent of holding it, even if only for a few years. Real estate investments do

not typically generate a return within several months or weeks; they

require an extensive waiting period in order for values to increase.

As a home

buyer, unless you're paying cash, you're likely to put some money down and take

out a loan, known as a mortgage, for the remainder of the

purchase price. There are different types of mortgages—fixed-rate and

adjustable are the most common—but the underlying principle is the same. You

pay off a little of the principal each month until you're left with ownership

of a debt-free asset that should continue to appreciate over time.

If you get a

fixed-rate mortgage, you end up paying off future debt with cheaper currency if

rates increase. But if rates decrease, you're still responsible for the fixed

amount. Various factors should be taken into account in order to determine your

best mortgage option.

Like land,

home prices tend to increase in value on an average year-over-year basis.

It is true that real estate bubbles are

usually followed by correctional periods, sometimes causing homes to lose over

half of their value. Still, on average, housing prices tend to increase over

time, counteracting the effects of inflation.

Invest in Yourself

By

far the best investment you can make to be prepared for an uncertain

financial future is an investment in yourself. One that will increase your

future earning power.

This

investment begins with quality education and continues with keeping skills

up-to-date and learning new skills that will match those most needed in the not-too-distant future. Being able to stay on top of a business's changing needs may

not only help to inflation-proof your salary, but also recession-proof your

career.

+++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++

Delta Air Lines: High Risk

Or High Reward?

Nov. 18, 2022 5:44 PM ETDelta Air Lines, Inc. (DAL)AAL, LUV, UAL4 Comments

Summary

- In an analysis on Delta Air Lines back

in August this year, I asked if the reward was worth the risk when

evaluating whether to invest in the company.

- At that time, I rated the Delta Air

Lines stock as a sell. Now, about 3 months later, I will tell you if I

come to a different conclusion.

- At the current stock price of $35, my

DCF Model shows an expected compound annual rate of return of 10% for the

company.

- In my opinion, the reward is still not

worth the risk, as I continue to see strong risk factors for investors.

- For these reasons, I maintain my sell

rating for the Delta Air Lines stock.

David

McNew

- Delta

Air Lines (NYSE:NYSE:DAL) has competitive advantages, which

help the company to build an economic moat over its competitors.

- The

company’s global airlines network and high necessary capital expenditures

lead to the fact that it is difficult for new competitors to

enter the airline industry.

- Delta

Air Lines’ EBIT Margin of 5.82% is higher than the one of United Airlines (UAL) (EBIT Margin of 2.01%)

and Southwest Airlines (LUV) (0.03%), underlying the company’s relatively strong

competitive position.

- At

the current stock price, my DCF Model indicates an Internal Rate of Return

of 10%; however, I continue to see a large amount of risk attached to a

Delta Air Lines investment. This leads me to the conclusion that the

reward you can achieve from investing in the company is not worth the

risk.

- If you do decide

to invest in the airline industry, I would recommend that you only invest

a maximum of 3% of your overall investment portfolio.

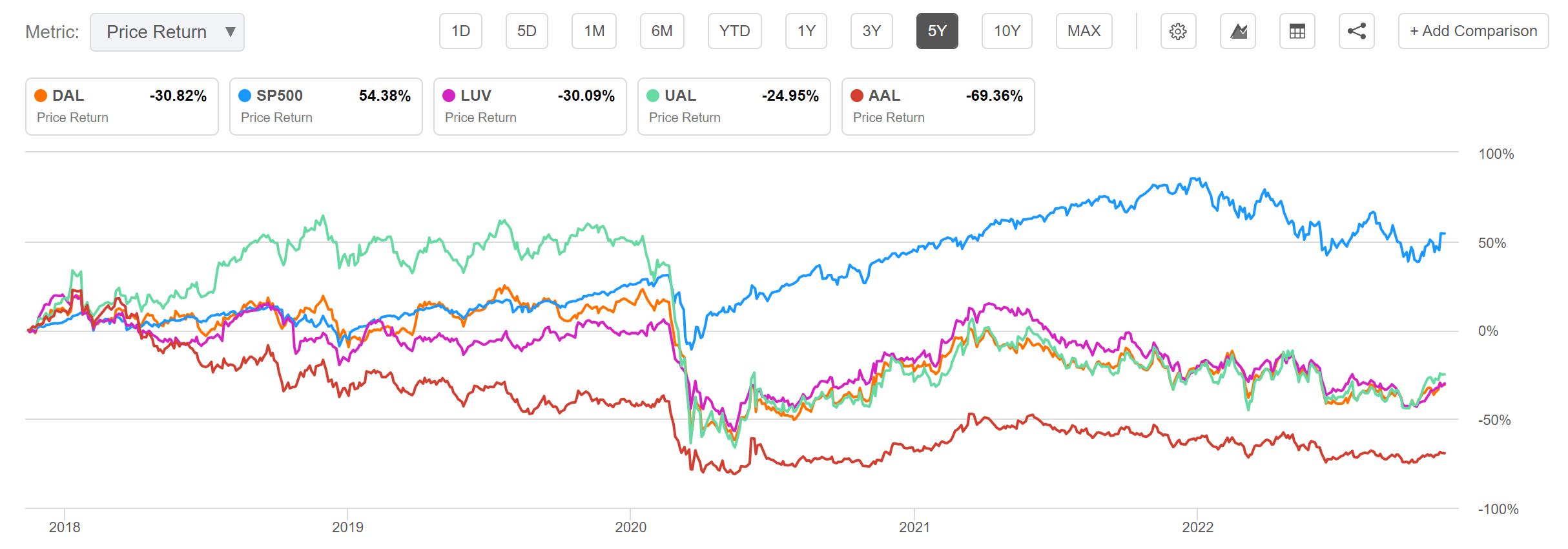

Delta Air Lines’ Stock Performance

The S&P 500 has shown a performance of 54.38% in the past 5

years as shown in the graphic below. The performance of Delta Air Lines

(-30.82%) as well as the performance of other companies from the same industry

such as Southwest Airlines (-30.09%), United Airlines (-24.95%) and American

Airlines (NASDAQ:AAL) (-69.36%) are significantly inferior when compared to

the performance of the S&P 500.

Even if no direct conclusions for the future can be drawn from the

past, history has shown that an investment in the S&P 500 (which is

associated with less risk due to the broad diversification) has generated a

significantly better return than any investments in these airline companies.

This strengthens my investment thesis that the reward is not worth

the risk when deciding to invest in Delta Air Lines or the airline industry in

general.

{kind=link}

Source:

Seeking Alpha

Delta Air Lines delivered strong 3Q22 results: the company

presented an operating revenue of $12.8B, implying an increase of 3% when

compared to the same quarter of 2019. At the same time, the airline company

revealed an operating income of $1.5B, implying an operating margin of 11.6%.

Ed Bastian, Delta's chief executive officer, commented on these

results with the following words:

"With strong demand and a

return to best-in-class operational performance, we are ahead of our plan for

the year on profitability and expect to be free cash flow positive. We're

working towards full network restoration by summer of 2023, which supports a

meaningful step up in profitability and cash flow next year on our path to earn

over $7 of EPS and $4 billion of free cash flow in 2024."

The Competitive Advantages and Growth Drivers of Delta Air Lines

In my previous analysis on Delta Air Lines back

in August, I showed that the company disposes of strong competitive advantages.

Due to this, I will only briefly discuss its competitive advantages in this

analysis. Among others, I mentioned the company's global network as a

competitive advantage:

“The company's global network

contributes to a strong competitive advantage. Delta Air Lines serves over 130

countries and territories as well as over 800 destinations around the world. At

the end of 2021, Delta Air Lines offered more than 4,000 daily departures to

its customers. Furthermore, the company's global network is supported by a

fleet of about 1,200 aircraft that vary in size and capabilities. This gives

the company flexibility to adjust aircraft to its existing network.”

In addition to the above, I mentioned in the same analysis that these

competitive advantages help the company to build an economic moat over its

competitors:

“The global network of Delta Air

Lines and other existing airline companies in combination with high necessary

capital expenditures (such as for aircraft leases and leases of airport property

and other facilities) contribute to the fact that it's extremely difficult for

new competitors to enter the industry.”

From my perspective, these competitive advantages contribute to

the fact that new competitors are unable to enter the market, but I don’t

identify strong growth drivers for Delta Air Lines' business, which contributes

to my sell rating for the company.

The Valuation of Delta Air Lines

Discounted Cash Flow [DCF]-Model

I have used the DCF Model to determine the intrinsic value of

Delta Air Lines. The method calculates a fair value of $34.61 for the company.

Its current stock price of $35.00 gives Delta Air Lines a downside of 1.1%.

My calculations are based on these assumptions as presented below

(in $ millions except per share items):

|

Delta Air Lines |

|

|

Company Ticker |

DAL |

|

Tax Rate |

30.0% |

|

Discount Rate [WACC] |

10.5% |

|

Perpetual Growth Rate |

2% |

|

EV/EBITDA Multiple |

9.9x |

|

Current Price/Share |

$35.00 |

|

Shares Outstanding |

638,2 |

|

Debt |

$31,936 |

|

Cash |

$7,023 |

|

Capex |

$5,384 |

Source: The Author

Based on the above, I have calculated the following results for

Delta Air Lines:

Market

Value vs. Intrinsic Value

|

Delta Air Lines |

|

|

Market Value |

$35.00 |

|

Downside |

1.1% |

|

Intrinsic Value |

$34.61 |

Source: The Author

Internal Rate of Return for Delta Air Lines

Below you can find the Internal Rate of Return as according to my

DCF Model. I assumed different purchase prices for the Delta Air Lines stock.

At Delta Air Lines’ current stock price of $35.00, my DCF Model

indicates an Internal Rate of Return of approximately 10% for the company. (In

bold you can see the Internal Rate of Return for Delta Air Lines’ current stock

price of $35.00.)

|

Purchase Price of the Delta

Air Lines Stock |

Internal

Rate of Return as according to my DCF Model |

|

$22.50 |

15% |

|

$25.00 |

14% |

|

$27.50 |

13% |

|

$30.00 |

12% |

|

$32.50 |

11% |

|

$35.00 |

10% |

|

$37.50 |

9% |

|

$40.00 |

9% |

|

$42.50 |

8% |

|

$45.00 |

7% |

|

$47.50 |

6% |

Source: The Author

Please note that the Internal Rates of Return above are a result

of the calculations of my DCF Model and changing its assumptions could result

in different outcomes.

The fact that my DCF Model indicates an expected compound annual

rate of return of 10% for Delta Air Lines, strengthens my belief that the

reward is currently not worth the risk when considering an investment in the

company. For this reward, I see too many risk factors attached. Therefore, I

reiterate my sell rating in regards to the Delta Air Lines stock. In the Risk

section of this analysis, I will describe these risk factors in more detail.

Delta Air Lines’ Fundamentals in comparison to its competitors

such as Southwest Airlines, United Airlines and American Airlines

At this moment in time, Delta Air Lines has a similar market

capitalization to Southwest Airlines: while Delta Air Lines’ market

capitalization is $22.20B, Southwest Airlines’ is $22.41B. However, Delta Air

Lines’ market capitalization is significantly higher than United Airlines’

($14.39B) and American Airlines’ (9.54B).

Delta Air Lines’ current EBIT Margin of 5.82% is higher than both

United Airlines’ (2.01%) and American Airlines’ (0.03%), but lower than

Southwest Airlines’ (7.16%). The generally low EBIT Margins of these companies

from the airline industry provides proof that an investment in this sector

comes with high risk factors. Declining revenues can result in losses, which in

turn can increase the probability of bankruptcy.

When it comes to growth, we can see that Delta Air Lines is

slightly ahead of its competitors: while Delta Air Lines has shown a Revenue

Growth of 2.92% over the last five years [CAGR], Southwest Airlines’ is 1.60%,

United Airlines’ 1.74% and American Airlines’ 1.58%.

In terms of Valuation, Delta Air Lines is slightly more attractive

than most of its competitors: while Delta Air Lines has a P/E Non-GAAP [FWD]

Ratio of 12.13, Southwest Airlines’ is 16.75 and United Airlines’ is 20.68. At

the same time, Delta Air Lines’ P/E Non-GAAP [FWD] Ratio is 29.39% lower than

the sector median, which is 17.18.

When it comes to risk, it can be highlighted further that Delta

Air Lines has a high Total Debt to Equity Ratio of 695.77%, which is a strong

indicator that the risk of investing in the company is very high. This once

again reinforces my belief that the reward is not worth the risk when

considering an investment in Delta Air Lines. The company’s Debt to Equity

Ratio is significantly higher than that of Southwest Airlines (92.57%), but

lower than United Airlines' (783.50%).

|

Delta Air

Lines |

Southwest

Airlines |

United

Airlines |

American Airlines |

||

|

General

Information |

Ticker |

DAL |

LUV |

UAL |

AAL |

|

Sector |

Industrials |

Industrials |

Industrials |

Industrials |

|

|

Industry |

Airlines |

Airlines |

Airlines |

Airlines |

|

|

Market Cap |

22.20B |

22.41B |

14.39B |

9.54B |

|

|

Profitability |

EBIT Margin |

5.82% |

7.16% |

2.01% |

0.03% |

|

ROE |

2.25% |

7.81% |

-14.56% |

NM |

|

|

Valuation |

P/E Non-GAAP [FWD] |

12.13 |

16.75 |

20.68 |

- |

|

Growth |

Revenue Growth 3 Year [CAGR] |

0.22% |

0.43% |

-1.67% |

-0.13% |

|

Revenue Growth 5 Year [CAGR] |

2.92% |

1.60% |

1.74% |

1.58% |

|

|

EBIT Growth 3 Year [CAGR] |

-24.52% |

-19.37% |

-43.23% |

-84.55% |

|

|

Income

Statement |

Revenue |

46.62B |

22.69B |

40.75B |

45.21B |

|

EBITDA |

4.47B |

2.72B |

3.09B |

2.40B |

|

|

Balance Sheet |

Total Debt to Equity Ratio |

695.77% |

92.57% |

783.50% |

NM |

Source: Seeking Alpha

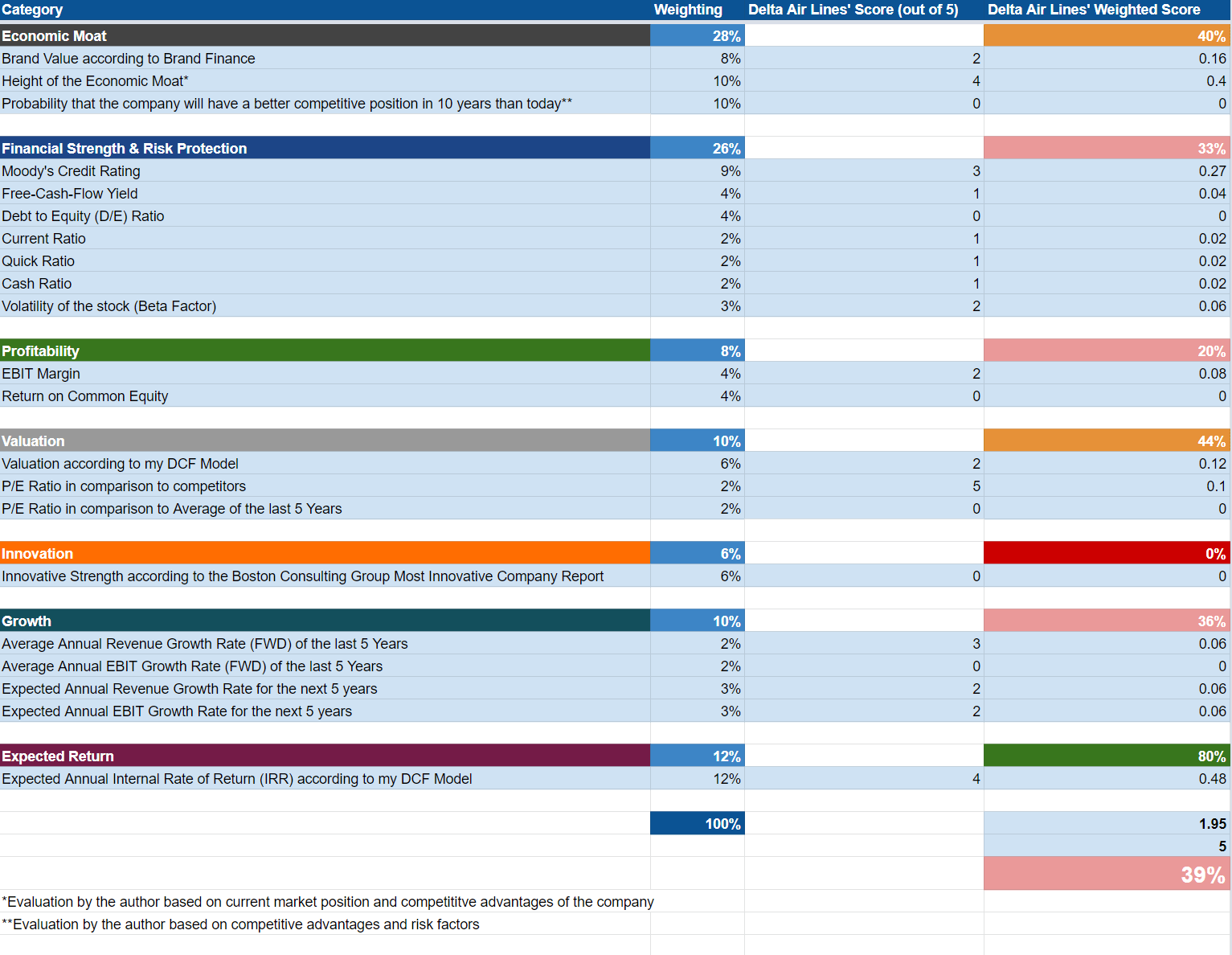

The High-Quality Company [HQC] Scorecard

"The HQC Scorecard aims to help investors identify companies

which are attractive long-term investments in terms of risk and reward."

Here, you can find a detailed description of how

the Scorecard works.

Overview of the Items on the HQC Scorecard

"In the graphic below, you can find the individual items and

weighting for each category of the HQC Scorecard. A score between 0 and 5 is

given (with 0 being the lowest rating and 5 the highest) for each item on the

Scorecard. Furthermore, you can see the conditions that must be met for each

point of every rated item."

{kind=link}

Source:

The Author

Delta Air Lines is rated as moderately attractive in the

categories of Valuation (44/100) and Economic Moat (40/100). For Growth

(36/100), Financial Strength (33/100) and Profitability (20/100), the company

is rated as unattractive. Only in the category of Expected Return, is the

company rated as very attractive (80/100).

Delta Air Lines’ unattractive overall rating (39/100), validates

my opinion to rate the company as a sell at this moment in time.

Risk Factors

From my point of view, there are plenty of risk factors investors

should take into consideration when thinking about investing in Delta Air

Lines:

In my previous analysis on Delta Air Lines, I discussed that the

financial results of companies from the airline industry vary widely depending

on the price of aircraft fuel:

“Increases in the cost of crude oil could have an adverse effect on

the company's operating results. Over time, fuel prices have been highly

volatile. Proof of this is the fact that from 2019 to

2021 the company's average annual fuel price per gallon varied from $1.64 to

$2.02. Year to year variations ranged from a decrease of 19% to an increase of

23%, as according to the company.”

Furthermore, I mentioned in my previous analysis that Delta Air

Lines might see a situation in which it can not meet its obligations:

“Additionally, Delta Air Lines has a significant amount of

existing fixed obligations (which includes, among others, aircraft lease and

debt financings, leases of airport property and other facilities). A disruption

to its business operations (which could be, for example, caused by another

pandemic) might see a situation in which the company isn't able to meet its

obligations.”

I also explained that consumer behavior has changed as a result of

the pandemic and that I do not expect it to return to the previous level:

“It can be assumed that the number of flights will not return to

pre-pandemic levels in the future due to companies having recognized the

advantages of virtual meetings and are therefore more likely to save on travel expenses.

As according to Reuters, Amazon (NASDAQ:AMZN)

alone saved $1 billion in travel costs during the pandemic.”

In addition to the risk mentioned above, Delta Air Lines’ high

Total Debt to Equity Ratio of 695.77% and its relatively low EBIT Margin of

5.82% demonstrate the high risk that is attached to an investment in the

company. This relatively high number of risk factors increases my confidence in

the theory that Delta Air Lines should be rated as a sell.

The Bottom Line

At this moment in time, I consider that the reward is not worth

the risk when considering to invest in Delta Air Lines. In the Risk section of

this analysis, I mentioned a large amount of factors that you need to take into

account before investing in the company. At the current stock price of $35, my

DCF model demonstrates an expected compound annual rate of return of 10% for

Delta Air Lines. From my point of view, this reward is not worth the

aforementioned risks; underlying my sell rating for the company.

In general, I don’t see the airline industry as being very attractive from an

investors perspective. This is especially due to the high-risk factors for

airline companies in general; however, if you decide to invest in Delta Air

Lines or in another company from the industry, I would suggest that you limit

your investment to a maximum of 3% of your total investment portfolio.

This article was written by

In my analyses,

I aim to identify companies that have strong competitive advantages over their

competitors (for example, a strong brand image, cost advantages, special know

how, strong pricing power, a strong distribution network, etc.) in order to

support you to find excellent long-term investments. I aspire to help you build

an investment portfolio consisting of high-quality companies that are

particularly attractive in terms of risk and reward (for example, due to their

wide economic moat, high financial strength, high profitability, attractive

valuation, growth potential and expected return). I was born in Germany and

majored in Business Administration at the University of Mannheim (Germany) and

San Diego State University (United States).

Show more

Disclosure: I/we have a beneficial long position in the

shares of AMZN either through stock ownership, options, or other derivatives. I wrote this article

myself, and it expresses my own opinions. I am not receiving compensation for

it (other than from Seeking Alpha). I have no business relationship with any

company whose stock is mentioned in this article.

(As with any of these informative articles,

anyone who needs someone to talk to about

this

very subject contact me and I can direct you to a knowledgeable advisor).

No comments:

Post a Comment